|

2. Benefit Plan 1 2.1 Database

2.1.1 PREVI has its own reference file for Benefit Plan 1 participants, which is integrated to the Entity’s other information systems. To compose this reference file, we receive financial and non-financial information (personal and functional data) from the Banco do Brasil and from the available database. The data are treated carefully, and submitted to consistency and reliability filters.

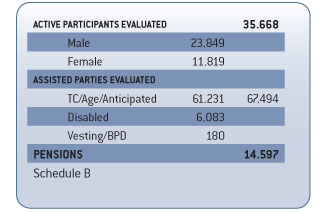

2.1.2 The reference file database that is used for the actuarial appraisal of Benefit Plan 1 dates to December 2008. The reference file’s summary shows the following active participant, assisted participant and pensioner figures:

2.2.1 On account of CGPC Resolution # 16, of 11/22/2005, and of SPC Normative Instruction # 9, of 01/17/2006, Benefit Plan 1 is established as a defined benefit plan. It is composed of a general part, aimed to all participants, based on the defined benefit mode, and of an optional part, which is additional to the general part, is based on the variable contribution mode, and has exclusive contributions made by the participant.

2.2.2 There are also special benefits, paid while the resources that are in the funds constituted to cover the respective benefits suffice to support them, as defined in Chapter XV of the Regulation.

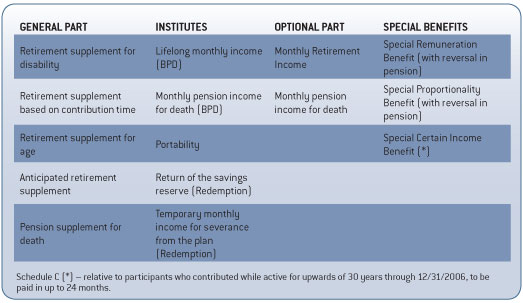

2.2.3 Schedule C shows the types of benefits provided by Benefit Plan 1:

2.3.1 Benefit Plan 1 is appraised based on the capitalization system for all regular benefits. The financial system that is used is capitalization and the actuarial method applied is the aggregate one, as provided for by item 5.1 of the Exhibit of CGPC Resolution # 18, of 03/28/2008.

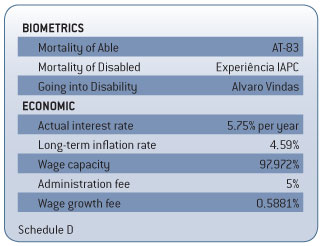

2.3.2 The premises used in the December 2008 actuarial reappraisal for the 2009 fiscal year were approved by the Executive Board and by the Deliberative Body. The approved premises were:

2.3.3 When comparing the current premises to those of the previous year, we notice there were changes in those that regard wage capacity and the wage growth rate. The capacity factor was reduced from 98.053% to 97.972% because of the change in scenario for the long-term inflation rate.

2.3.4 The wage growth rate, which reflects the projection of the active participants’ wages when they start receiving the benefit, was changed from 0.8394% to 0.5881%, as per a report prepared by the sponsor.

2.4 Reserve to amortize2.4.1 Benefit Plan 1 has Reserves to Amortize on account of the financial cash flow coverage relative to participants hired by Banco do Brasil through 04/14/1967, and including, called Group-67. This is covered by the Agreement signed between Banco do Brasil and PREVI on 12/24/1997. On 12/31/2008, the amount of the Reserve to Amortize was R$12,095,121,253.67.

2.4.2 The Funding Plan to finance the Reserve to Amortize was determined by the mentioned Agreement, and PREVI is in charge of measuring the social security commitment, which appears in the Accounting and Actuarial Balance as 53.6883529% of the total retirement charge for Group-67.

2.4.3 The Tenth Clause of the Agreement determines that the Agreement’s term is tied to the liquidation of the last commitment for participants of Group-67’s retirement supplements.

2.5 Financial and actuarial status

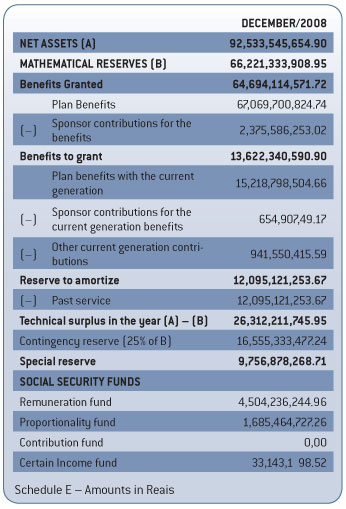

2.5.1 Schedule E shows the results of the actuarial appraisal carried out regarding the commitments taken on by the plan and its Net Assets on 12/31/2008:

2.5.2 The following Social Security Funds were created in December 2007 for the payment of special benefits, and the fund reversal rules appear in Chapter XV of the plan’s Regulation:

-

• Remuneration Fund: composed of resources derived from the Special Reserve, calculated actuarially for the payment of the Special Remuneration Benefit.

-

• Proportionality Fund: composed of resources derived from the Special Reserve, calculated actuarially for the payment of the Special Proportionality Benefit.

• Certain Income Fund: composed of resources derived from the Special Reserve, based on financial calculations, for the payment of the Special Certain Income Benefit.

2.5.3 There is also the Contribution Fund, created in July 2007, composed of resources derived from the Special Reserve, accounting in nature, formed as a result of the budget forecast, created for the payment of personal and employer contributions during the year.

2.5.4 As a result of the performance of the investment assets and the normal evolution of the social security liability, an accumulated technical surplus of R$26,312,211,745.95 was calculated, constituting a Contingency Reserve equivalent to R$16,555,333,477.24 and a Special Reserve for Plan Revision ofR$9,756,878,268.71.

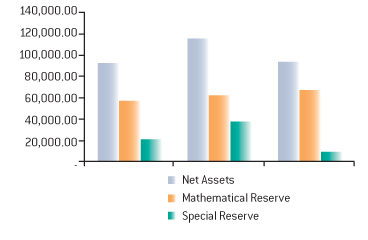

2.5.5 The following is the evolution of the Mathematical Reserves and of the Net Assets of Benefit Plan 1 in the past three years (amounts in R$ million):

2.6.1 The Funding Plan determines the contribution level that is required to fund the plan’s benefits according to the financial system and the funding method in order to maintain the plan’s balance and solvency.

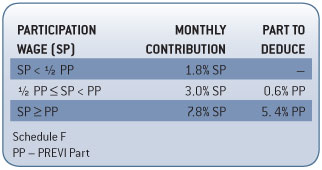

2.6.2 Benefit Plan 1 is financed by the monthly and annual contributions made by the active participants, retirees, and by the sponsor. The active participants’ contributions are calculated based on their participation wage, as per Schedule F:

2.6.3 The average active participant contribution percentage is 6.66% of the participation wage. In the case of retired participants, the contribution percentage is 4.8% of the retirement supplement.

2.6.4 The Regulation in effect, as approved by the Office of Supplemental Pension Plans (SPC) on 12/19/2007, determined the temporary suspension of personal and employer contributions for the General Part of Benefit Plan 1. The suspension is renewed annually as long as there is a Special Reserve from the previous year.

2.6.5 To fulfill the provisions set forth by the Regulation, the Contribution Fund was constituted in 2007 with an amount equivalent to the contributions of the 2007 fiscal year – R$675,000,000 – based on the amount estimated for the year.

2.6.6 For 2008, the Contribution Fund received subsidies of R$702,307,000 to substitute for the contributions made by the participants and by the sponsors in the period.

2.6.7 The amount estimated for 2009, relative to personal and employer contributions for Benefit Plan 1, is R$752,633,686.00. As can be seen in items 2.5.3 and 2.6.4, there is a big enough balance in the Special Reserve calculated on 12/31/2008 to keep the suspension of normal contributions made by both participants and sponsors.

2.7 Actuarial gains and losses2.7.1 These are the differences between the projected actuarial premises for the year and the actual experience in the period. Based on the comparison of the attained and expected amounts for Benefit Plan 1, we noticed the following factors varied the most:

-

• Change in the Actuarial Premises: as mentioned in items 2.3.3 and 2.3.4, the premises relative to the wage growth rate and the capacity factor changed between 2007 and 2008. The difference between the premises generated a reduction in the Mathematical Reserve in the amount of R$254,884,318.32.

• Participants in Imminent Risk: There are some 9,800 participants who, even after fulfilling the requirements to get the scheduled benefit (especially the anticipated benefit), remain in the Plan as active participants. This fact generated an actuarial gain for the plan of R$303,867,878.14.

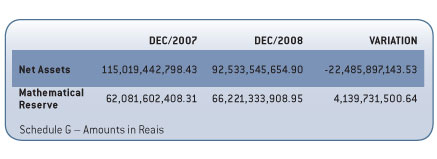

• Calculated Profitability x Actuarial Goal: the actuarial goal for 2008, equivalent to the sum of the INPC from January to December and the 5.75% interest rate, corresponded to 12.60%; however, the performance of the plan’s investment asset was -11.49%. Schedule G shows Net Asset variations that include Plan 1’s negative profitability (R$15.7 billion) and the disbursement for benefit payments (R$6.2 billion), in addition to the Mathematical Reserve during 2008:

1 Valor apurado sobre o Ativo Bruto

em 31/12/2007 (R$ 137,1 bilhões).

2.8.1 CGPC Resolution No. 26

2.8.1.1 On 09/29/2008, the Supplemental Pension Plan Management Council (CGPC) approved CGPC Resolution # 26, which provides on the conditions and procedures to be observed by the entities while calculating results, while allotting amounts and while using the surplus. The hypotheses that should be considered in the appraisal’s calculation in the event of Benefit Plan revisions are:

-

• Adoption of the AT-2000 Mortality of Able Table;

• Adoption of the Actual Interest Rate of 5% per year.

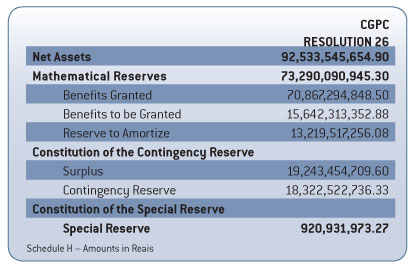

2.8.1.2 Considering the above-mentioned hypotheses, for illustration purposes, we present the result calculation amounts in Schedule H:

2.8.1.3 The resolution also determines that, for benefit plans that are executing the investment matching plan for their guarantee resources, , for calculation purposes the allotment of the special reserve may only take place if the accumulated surplus result is deduced from the total amount equivalent to the mismatching, which in December 2008 corresponded to R$12,473,229,007.69.

2.9 Conclusion2.9.1 The amounts calculated for the Mathematical Provisions and the Social Security Funds, and the evolution that is expected for the commitments taken-on by the Plan regarding its participants showed that the actuarial premises were defined appropriately for the period under analysis; therefore, we recommend the Funding Plan in effect for Benefit Plan 1 be maintained.

2.9.2 Considering item 2.6.7, we believe the personal and employer contribution collection suspension should be maintained for 2009, reconstituting the Contribution Fund based on the annual budget for participant and sponsor contributions, without any impact on the Funding Plan.

2.9.3 Considering the above, we conclude the results attained by the Plan at the closing of the 2008 fiscal year indicate it is actuarially balanced.